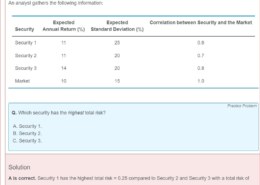

I had a smiler doubt. Therefore I calculated BETA of each security with respect to market and since security 1’s beta was 1, security 2’s beta was 1.067 and security 3’s beta was 0.93. Now seeing all securities SD, Concluded that Security A has the highest total risk considering the percentage change in systematic risk of both security 1 & 2’s BETA (of 6.67%) and percentage change in unsystematic risk of both security 1 &2’s SD (of 25%).

I am not sure how much this logic is true but answer was correct.

I had a smiler doubt. Therefore I calculated BETA of each security with respect to market and since security 1’s beta was 1, security 2’s beta was 1.067 and security 3’s beta was 0.93. Now seeing all securities SD, Concluded that Security A has the highest total risk considering the percentage change in systematic risk of both security 1 & 2’s BETA (of 6.67%) and percentage change in unsystematic risk of both security 1 &2’s SD (of 25%).

I am not sure how much this logic is true but answer was correct.