In questions of expected share price and expected value of options, we calculated the expected price of share by normal probably distribution method i.e by following way

Sum of (Expected price × probability)

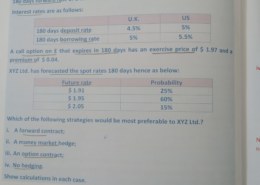

However in the sums of option hedging (image attached), while calculating the expected buying rate of pound we fixed the buying rate at lower of St or x against each probability?

Why two different ways of calculating the same thing?

Hey Ayushi!

Expected price of share is calculated as you mentioned that is, Sum of expected price * Probability. This is because share’s price is not being dependent on any underlying asset, is it?

While that is not the case with Options (being derivatives). It depends on the share price as well as on strike price at which you paid your premium. Keeping it short, If my share price exceeds the strike rate, i will exercise my option and get the amount and when it doesnt, i would not exercise and my payoff against it will be Zero. Hence, the value of option is the payoff i get, right? So if my Strike price was 150 and my share price is 160, value of my option is Rs. 10. Probablity of the investor getting Rs. 10 is lets say, 60%. Hence, we see all the prices individually for deriving the value one might get. I was like to bring your attention to all the questions asked for valuing option with expected prices of shares given. They have ALWAYS asked price at maturity. Please check for your satisfaction. And as you know, at maturity, there is no time value of money only intrinsic value and hence, Strike price is compared with share price and value is derived.

So simply calculating sum of expected prices * probability wont work because not every future rate you will get payoff. Hence, you will check at individual prices, calculate payoff and multiply the probability.

Hope your doubt got cleared. All the best! :))