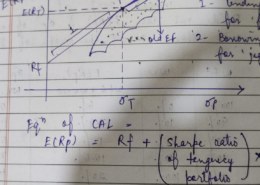

Why the tangency is considered as optimum point, old EF is set of all risky assets where as CAL is risky and Rf.

Please briefly explain why you feel this question should be reported.

Please briefly explain why you feel this answer should be reported.

Please briefly explain why you feel this user should be reported.

Why the tangency is considered as optimum point, old EF is set of all risky assets where as CAL is risky and Rf.

Tangency is considered to be the optimum point as it’s the point at which your EF touches the tangent which provides you with optimum level of return with the desired risk level.

If you choose a point below it, it means you’re lending at rf generally a highly risk averse investor does this whereas, if you choose a point above the tangent, you’ll be borrowing at rf and investing at the risky asset which a high risk appetite person does.

Hope this helps!

How this borrowing and lending thing came here?

You may have not come across it, as you move forward you’ll find Sir teaching us this. Thank you.