When calculating Bond price at any node, we do it via backward induction, isn’t it?

Then why in this sum has 102.2 been divided directly by the lower node rate in T=1 (1.7635%)??

PART of QUESTION IS GIVEN BELOW:

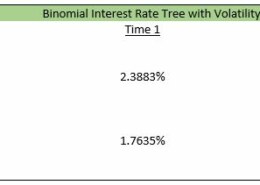

Based on binomial trade movements in Exhibit 3 and Exhibit 4, CanBank Bond’s value at the lower node in Time 1 is closest to:

A$100.89

B$99.82

C$100.43 Correct Answer

Because it’s a 2 year bond, total CF at the end of year 2 will be 102.2

Value of the bond at lower node= 102.2/1.017635 = 100.43

Oh right! What sir calls a 2 period binomial tree, institute considers it 3. That was the confusion.

Thanks