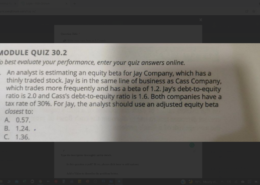

0 Aarush GoelIntermediate Asked: November 20, 20212021-11-20T21:15:32+05:30 2021-11-20T21:15:32+05:30In: Corp. Finance (CFA L1) cost of capital 0 what should be the answere?? Share Sorry, you do not have permission to answer to this question. 4 Answers Oldest Vishwajeetsinh Jadeja01 The Official Nerd 2021-11-20T21:35:35+05:30Added an answer on November 20, 2021 at 9:35 pm Cass’s D/E = 1.6 and Levered Beta = 1.2 We need to deleverage this to get the business risk. Thus, Cass’s unlevered Beta = (Beta) / (1 + (D/E)(1-t)) = 1.2 / (1 + (1.6*0.7)) = 0.566 Thus, to get Jay’s Beta, we need to re-leverage this with Jay’s D/E: Levered beta = Unl Beta * (1 + (D/E)(1-t)) = 0.566 * (1 + (2 * 0.7)) = 1.36 Thus, answer is C. Aarush Goel Intermediate 2021-11-20T21:50:26+05:30Replied to answer on November 20, 2021 at 9:50 pm is other any difference between adjusted and unadjusted Equity beta?? roshani.dubey@2020 Advanced 2021-11-20T22:37:38+05:30Added an answer on November 20, 2021 at 10:37 pm Yes , unadjusted equity beta does not consider the project risk whereas adjusted equity beta takes into account the project risk . Aarush Goel Intermediate 2021-11-20T22:50:07+05:30Replied to answer on November 20, 2021 at 10:50 pm how to calculate that??

Cass’s D/E = 1.6 and Levered Beta = 1.2

We need to deleverage this to get the business risk. Thus, Cass’s

unlevered Beta = (Beta) / (1 + (D/E)(1-t)) = 1.2 / (1 + (1.6*0.7)) = 0.566

Thus, to get Jay’s Beta, we need to re-leverage this with Jay’s D/E:

Levered beta = Unl Beta * (1 + (D/E)(1-t)) = 0.566 * (1 + (2 * 0.7)) = 1.36

Thus, answer is C.

is other any difference between adjusted and unadjusted Equity beta??

Yes , unadjusted equity beta does not consider the project risk whereas adjusted equity beta takes into account the project risk .

how to calculate that??